The Most Millennial Spending Habits

Millennials now make up the nation’s largest generation and are beginning to transition into their prime earning (and spending) years. Now the most populous generation, and soon to be the nation’s biggest spenders, it’s fitting that millennials seem to dominate conversations around product strategy, marketing, and the economy at large.

Whether millennials will ultimately be better or worse off financially than their parents is still up for debate. What’s clear, though, is that millennials represent a new breed of consumer that are in a different spot financially than preceding generations, affecting everything from how they talk about money to how they spend it.

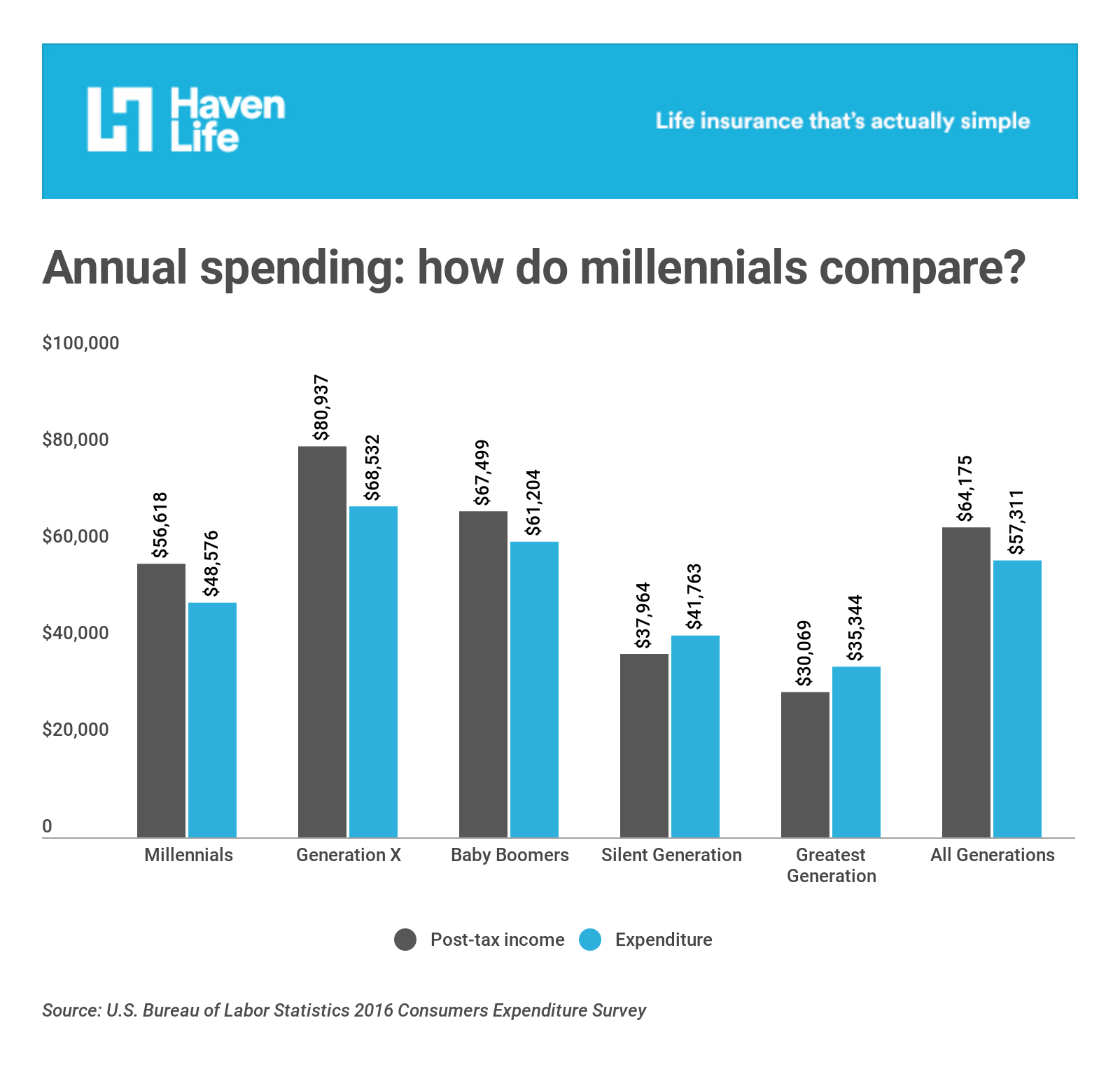

To better understand how millennial consumers compare to their parents, researchers at Haven Life, an online life insurance agency, analyzed data from the U.S. Bureau of Labor Statistics Consumer Expenditure Survey. The Consumer Expenditure Survey (CE) is a nationwide household survey that tracks how Americans spend across a variety of goods and services that are grouped into broad categories such as housing, transportation, and healthcare. Overall income and spending figures are shown below.

Of course, because millennials are earlier in their careers, it’s expected that they have lower incomes than their parents, and thus, lower absolute spending on most items. This is why expenditure share—the ratio of spending on a given item to total spending across all items—is a more useful metric of comparison than absolute spending is alone.

Below, Haven Life’s researchers highlight the categories where millennials outspend, underspend, and spend the same as their parents—who, for the purpose of this report, are defined as members of Generation X and baby boomers. Certain spending differences, such as renting vs. owning housing costs, might be the temporary result of current age differences across generations, and will likely be “corrected” over time. Conversely, other spending habits could be the result of permanent cultural and demographic differences that will likely impact millennial financial decisions throughout their life. For example, millennials are more highly educated than any preceding generation, and will continue paying off higher education costs far later in life than did previous generations.

While this analysis focuses on how millennials spend differently from their parents today, it will be important to watch how these trends change, or stay the same, in the coming years.

Where millennials outspend their parents

Photo Credit: Katarzyna Bialasiewicz / Alamy Stock Photo

1. Housing

- Millennial expenditure share: 34.9% ($16,959 annually)

- Generation X expenditure share: 33.1% ($22,669 annually)

- Baby boomer expenditure share: 30.9% ($18,917 annually)

The cost of housing is going up and it appears to be affecting millennials, who are less likely to own homes or to have recently bought, more than it’s affecting their parents. At 34.9 percent, millennials spend a greater share of their expenses on housing than older generations do (33.1 percent for Generation X and 30.9 percent for baby boomers).

However, the category “housing,” as defined by the Consumer Expenditure Survey, is broad and encompasses a variety of housing-related expenses and types of living spaces. Within the housing category, millennials outspend for rented dwellings and underspend for owned dwellings. Also within the housing category, millennials outspend on what the BLS defines as “personal services,” which include babysitting and childcare (in fact, some sources estimate childcare expenses for millennial parents to be north of $10,000 per year). Additionally, the BLS groups phone services in the broader housing category. With landline usage becoming less common, millennials underspend on residential phone services and outspend on cell phone services.

Photo Credit: scorton / Alamy Stock Photo

2. Transportation

- Millennial expenditure share: 17.3% ($8,426 annually)

- Generation X expenditure share: 15.4% ($10,545 annually)

- Baby boomer expenditure share: 15.9% ($9,762 annually)

Overall, transportation is the second-highest expense category for all three generations. Millennials tend to spend more than Generation X and baby boomers on vehicles, used cars and trucks, vehicle finance charges (such as the interest for an auto loan), vehicle rentals and leases, and gas. Interestingly, millennials spend less than their parents on public transportation, such as mass transit, buses, trains, and airlines, as well as vehicle insurance.

Photo Credit: Cropper / Alamy Stock Photo

3. Food away from home

- Millennial expenditure share: 6.1% ($2,946 annually)

- Generation X expenditure share: 5.9% ($4,040 annually)

- Baby boomer expenditure share: 5.1% ($3,100 annually)

In 2017, an Australian millionaire blamed millennials’ overspending on culinary luxuries like avocado toast for their inability to own homes. Though this is an oversimplification, the BLS data supports that millennials like to eat out. As a percentage of expenditure, millennials spend more than Generation X and baby boomers on food away from home (6.1 percent, compared to 5.9 percent and 5.1 percent). This includes meals, drinks, and snacks at restaurants, concession stands, vending machines, meal plans at schools, and take-out and delivery. However, the BLS report also notes that expenses for food away from home has historically declined with age. For instance, retired persons are not buying food during a lunch break and therefore would spend less on food away from home than someone who is currently in the workforce and eats out with co-workers. We will have to wait and see if millennial spending in this category will decrease as quickly as it has for previous generations or remain high.

Photo Credit: JG Photography / Alamy Stock Photo

4. Education

- Millennial expenditure share: 3.4% ($1,645 annually)

- Generation X expenditure share: 2.6% ($1,756 annually)

- Baby boomer expenditure share: 2.1% ($1,295 annually)

With 71 percent having a college degree, millennials are more highly educated than any preceding generation. The combination of increased educational attainment and dramatic tuition increases over the past few decades means that millennials spend a greater percentage of income than earlier generations on educational expenses.

Photo Credit: Lumi Images / Alamy Stock Photo

5. Alcoholic beverages

- Millennial expenditure share: 0.9% ($461 annually)

- Generation X expenditure share: 0.8% ($552 annually)

- Baby boomer expenditure share: 0.8% ($518 annually)

Millennials spend slightly more than Generation X and baby boomers on alcoholic beverages, which include beer and ale, wine, whiskey, gin, vodka, rum, and other liquors. Millennials spend $461 per year (0.9 percent), compared to Generation X’s $552 and baby boomers’ $518 (both 0.8 percent). Millennials are more likely than other generations to experiment with different types of alcoholic beverages, with craft beer being extremely popular among this demographic.

Where millennials underspend their parents

Photo Credit: Hero Images Inc. / Alamy Stock Photo

1. Personal insurance and pensions

- Millennial expenditure share: 11.9% ($5,768 annually)

- Generation X expenditure share: 13.2% ($9,015 annually)

- Baby boomer expenditure share: 13.0% ($7,976 annually)

Millennials spend 11.9 percent of their expenditures on personal insurance and pensions, more than a full percentage point less than their parents. Within this broad category, millennials also spend the least on pensions and Social Security, as well as life and other personal insurance. This is consistent with Haven Life’s recent survey on millennial parents, which found that 20 percent have no life insurance at all, and of those who did, 70 percent are underinsured.

Photo Credit: Sean Pavone / Alamy Stock Photo

2. Healthcare

- Millennial expenditure share: 5.1% ($2,473 annually)

- Generation X expenditure share: 6.6% ($4,492 annually)

- Baby boomer expenditure share: 9.0% ($5,492 annually)

Perhaps not surprising, healthcare costs increase with age. Millennials spend less than Generation X on healthcare (5.1 percent compared to 6.6 percent) and significantly less than baby boomers (9.0 percent). Within the larger category of healthcare, millennials have the lowest expenditures for health insurance; medical services such as x-rays, lab tests, eye and dental care, nursing home care, and hospital services; and drugs. With constant changes to the healthcare system, insurance requirements, and healthcare costs, it will be interesting to see how this category changes as millennials age.

Photo Credit: Scott Wilson / Alamy Stock Photo

3. Entertainment

- Millennial expenditure share: 4.8% ($2,311 annually)

- Generation X expenditure share: 5.3% ($3,613 annually)

- Baby boomer expenditure share: 5.1% ($3,144 annually)

Despite millennials’ reputation for overspending on “lifestyle” and trying to keep up with friends, they actually spend less than their parents on entertainment, which includes fees and admissions, audio and visual equipment and services, pets, toys, hobbies, and playground equipment. Millennial expenditures for entertainment are 4.8 percent, while for Generation X they are 5.3 percent and for baby boomers they are 5.1 percent. Within the entertainment category, millennials spend the least on pets, as well as fees such as club memberships and admission to events such as sports, movies, concerts, and plays.

Photo Credit: Tetra Images / Alamy Stock Photo

4. Cash contributions

- Millennial expenditure share: 2.1% ($1,007 annually)

- Generation X expenditure share: 2.8% ($1,936 annually)

- Baby boomer expenditure share: 4.4% ($2,717 annually)

Millennials spend less on the category defined as cash contributions than Generation X and baby boomers. Cash contributions include cash given to persons or organizations outside the household, and might include alimony and child support payments and charitable donations. Overall, millennials allocate 2.1 percent ($1,007 per year) here, compared to Generation X’s 2.8 percent ($1,936 per year) and baby boomers’ 4.4 percent ($2,717).

Photo Credit: Cultura Creative (RF) / Alamy Stock Photo

5. Gifts

- Millennial expenditure share: 1.1% ($541 annually)

- Generation X expenditure share: 1.6% ($1,119 annually)

- Baby boomer expenditure share: 2.7% ($1,669 annually)

Similar to cash contributions, gifts are expenditures given to persons outside of the household. However, rather than cash, these are tangible goods or services and are assigned an appropriate market value for the purpose of determining expenditure share. Millennials dedicate 1.1 percent of expenditures to gifts, while Generation X dedicates 1.6 percent and baby boomers dedicate 2.7 percent. While the data doesn’t show who the gifts are going to, it is likely that Generation X and baby boomers are spending on their millennial children in the form of paying for their education, vehicles, clothes, food, and more.

Photo Credit: Carolyn Franks / Alamy Stock Photo

6. Reading

- Millennial expenditure share: 0.1% ($64 annually)

- Generation X expenditure share: 0.2% ($115 annually)

- Baby boomer expenditure share: 0.2% ($130 annually)

Millennials underspend parents on reading materials, spending $64 annually (0.1 percent of expenditures) compared to Generation X and baby boomers spending $115 (0.2 percent) and $130 (0.2 percent), respectively. Reading includes paid newspapers and magazines; books through book clubs; e-books; and encyclopedias and other reference books. Notably, this does not necessarily mean that millennials are reading less. In fact, millennials are the most likely generation to use public libraries, and they are increasingly getting content for free online rather than paying for traditional print media.

Where millennial spending is consistent with their parents

Photo Credit: Image Source / Alamy Stock Photo

1. Food at home

- Millennial expenditure share: 6.9% ($3,370 annually)

- Generation X expenditure share: 7.0% ($4,830 annually)

- Baby boomer expenditure share: 6.9% ($4,224 annually)

Percentage-wise, millennials spend about as much on groceries as Generation X and baby boomers. Millennials allocate 6.9 percent of their expenditures ($3,370 annually) to food at home, which is the same as baby boomers and 0.1 percent lower than Generation X. Shares are the same across a wide range of grocery items, with the exception of fresh milk and cream, which millennials appear to have an affinity for.

Photo Credit: EyeEm / Alamy Stock Photo

2. Apparel and services

- Millennial expenditure share: 3.6% ($1,753 annually)

- Generation X expenditure share: 3.8% ($2,577 annually)

- Baby boomer expenditure share: 2.6% ($1,602 annually)

Millennials spend about the same percentage on apparel and services as Generation X (3.6 percent compared to 3.8 percent), and a little more than baby boomers (2.6 percent). Millennials outspend the other generations on apparel for men over 16 and children under 2, which makes sense since they are more likely to have young children. Apparel and services include clothing items, such as coats, sweaters, jackets, blouses, dresses, shorts, pants, undergarments, and footwear. Services that fall into this category include dry cleaning, tailoring, alterations, shoe repair, jewelry repair, and more.

Photo Credit: Oleksii Shynkevych / Alamy Stock Photo

3. Personal care products and services

- Millennial expenditure share: 1.2% ($563 annually)

- Generation X expenditure share: 1.2% ($826 annually)

- Baby boomer expenditure share: 1.2% ($756 annually)

For personal care products and services, there isn’t much variation across generations. Millennials, Generation X, and baby boomers all allocate 1.2 percent of expenditures to personal care products and services. This category encompasses hair care, oral hygiene, shaving products, cosmetics, bath products, electric personal care appliances (electric razor, electric toothbrush, etc.), and personal care services for men and women.

4. Tobacco products and smoking supplies

- Millennial expenditure share: 0.6% ($313 annually)

- Generation X expenditure share: 0.6% ($399 annually)

- Baby boomer expenditure share: 0.6% ($386 annually)

Despite the long-term decline in smoking rates over the past several decades, members of all three generations still spend, on average, a few hundred dollars each year on tobacco products and smoking supplies. This represents a consistent 0.6% of total spending for millennials and their parents.

Methodology

The data used in this analysis is from the U.S. Bureau of Labor Statistics 2016 Consumer Expenditure Survey. The survey and this analysis look at current spending patterns across generations, not how age-adjusted generational spending habits differ.

For each spending category, current annual expenditure shares were evaluated across three generations—millennial (birth year of 1981 or later), Generation X (birth year from 1965 to 1980), and baby boomer (birth year from 1946 to 1964). Expenditure shares are the ratio of expenditures on a given item or in a given category of items to the sum of expenditures on all items. When the millennial expenditure share was the lowest across the three generations, it was considered a category in which millennials underspend their parents. Conversely, when the millennial expenditure share for a given category was the highest, it was considered a category in which millennials outspend. The spending categories are ordered by their respective millennial expenditure shares. Total annual expenditures are also shown.

While detailed spending statistics are not provided for the silent generation (birth year from 1928 to 1945) or the Greatest Generation (birth year of 1927 or earlier), these generations are included in certain charts and figures.

Haven Life Insurance Agency LLC (Haven Life) conducted this research for educational/informational purposes only. Haven Life is an online life insurance agency offering term life insurance issued by Massachusetts Mutual Life Insurance Company. Haven Life does not provide tax, legal, investment, or housing/real estate advice, and the information in the study should not be relied on as such. You should consult your own tax, legal, investment, and other advisors, as appropriate, before engaging in any transaction.

More From 92.9 The Lake